The prospect of the taxman taking a substantial chunk of your hard-earned income is never a pleasant one. For residents in Scotland earning above £75,000, a new tax threshold alongside an increase to the Top rate of tax announced in last month’s Scottish budget may leave many feeling uneasy. In this article we will expand on these changes, including the “67.5% tax trap” facing some Scottish taxpayers, and how this can be mitigated.

Understanding Scottish Tax Bands

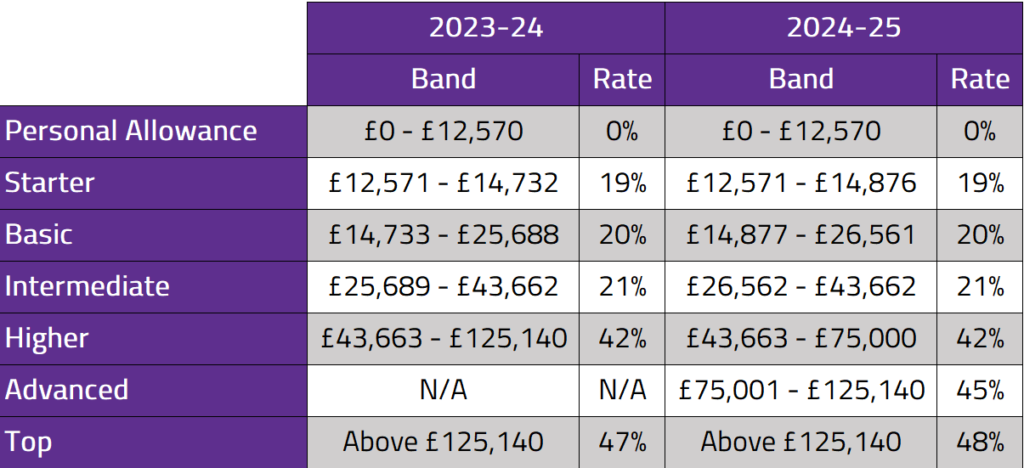

Scotland’s Income Tax system is already more complex than other parts of the UK, featuring five thresholds and the highest top rate among the four nations. From April 2024, the introduction of a sixth rate (the Advanced rate) will mean that 45% tax will be charged on earnings between £75,000 and £125,140. The top rate of Income Tax (for those earning over £125,140) will also increase from 47% to 48%. The table below compares the current tax year Income Tax rates and bands to the proposed changes for the upcoming 2024/25 tax year:

Impact of Changes

Impact of Changes

So, what is the expected impact of these proposals on Scottish taxpayers? For those earning under £75,000 the good news is that they will keep slightly more in their pockets with the Basic and Intermediate rates being raised by 1% and 3.4%, respectively. However, as these increases are below the rate of inflation, those in these brackets will still see a reduction in their real income (and therefore their purchasing power) as a result.

The proposed changes are obviously unwelcome news for the estimated 114,000 workers who will pay the new Advanced rate, as well as the further 40,000 who are projected to pay the Top rate of tax.

The 67.5% Tax Trap

For those earning above £100,000, the combined effect of the 45% Advanced rate and the gradual taper of the tax-free Personal Allowance (by £1 for every £2 of earnings above £100,000) can create a significant tax burden. In the current 2023/24 tax year, the taper of the Personal Allowance means that Scottish taxpayers are taxed at an effective rate of 63% for earnings between £100,000 and £125,140. With the introduction of the new 45% Additional rate in Scotland at the start of the upcoming 2024/25 tax year, this effective rate of tax will increase to a staggering 67.5%.

The situation is somewhat more palatable for high earners in the rest of the UK where lower rates of tax mean individuals within this income bracket are ‘only’ subject to the “60% Tax Trap”. Of course, things might change for those living outside Scotland; under pressure to reduce Income Tax burdens, we await to see the results of Chancellor Jeremy Hunt’s Spring Budget on 6th March 2024.

Avoiding the 67.5% Tax Trap

Navigating Scotland’s complex taxation regime requires strategic planning. High earners can explore various options to reduce their tax liability including tax-efficient investments, pension contributions, and claiming Higher rate gift aid on eligible charitable donations.

Let us look a bit more into the tax benefit of pension contributions, taking the example of a Scottish Taxpayer who earns £125,000 in the current 2023/24 tax year and as a result has lost £12,500 of their Personal Allowance due to the taper. A £20,000 contribution to a Personal Pension would immediately receive Basic rate tax relief and be grossed up by 25% to £25,000 in their pension. This contribution reduces their earnings, ‘Adjusted Net Income’ (ANI) for our purposes, by the gross amount of £25,000, resulting in an ANI of £100,000. This re-instates their entire Personal Allowance resulting in a further tax saving of £5,250 (42% of £12,500). They will also be entitled to claim Higher rate tax relief of £5,500 on their gross pension contribution (22%, the difference between Higher and Basic rate on the £25,000). The combined total of this equals a significant £15,750 tax saving (£5,000 + £5,250 + £5,500); equivalent to 63% of the gross £25,000 pension contribution.

In the same scenario above, but in the upcoming 2024/25 tax year, the £20,000 net pension contribution would result in a total tax saving of £16,875 (67.5% of gross £25,000).

Conclusion

As Scotland introduces new tax thresholds, high earners face the challenge of navigating a complex and high tax environment. Recent changes such as increasing the pension Annual Allowance from £40,000 to £60,000, and the planned abolishment of the Lifetime Allowance, offers savers more flexibility and incentive to save efficiently for retirement through strategic planning. If you wish to explore the impact these strategies might have for you personally, alongside the peace of mind and security that holistic Financial Planning can bring, please don’t hesitate to contact us.

Disclaimer:

The above article is for information only. You should not construe any such information or other material as tax, investment, financial, or other advice.