What’s fuelling ESG investment growth?

As the inexorable rise of ESG investing continues, we wanted to set out why we believe it is much more than investment marketing hutzpah, spin, or hype. We have been working closely with our investment partners in researching this subject for some time. Our conviction is that ESG principled investing is credible, effective, and financially rewarding. We have written on this topic before and will continue to share current thinking and activity in this area. It’s important we communicate our conviction and opinion to you. As you know, we tend to do things properly, not quickly. As the saying goes you can have it good, fast, or cheap; but you can only pick two.

So, why all this fuss over some “Johnny come lately” investing fad? Firstly, ESG methodology is not new. It goes back to 1972 and the formation of the UNEP (United Nations Environmental Programme). The UNEP FI (Finance Initiative) followed in 1992 stimulating global banking collaboration on environmental and sustainable development. Its rich heritage of championing change continues today. Since then, the original 28 banks and UNEP have grown into a unique public-private partnership with 1500 signatories from over 50 countries and $60 trillion. Global banks were joined by global insurers in 1999, creating a critical mass of influencers that would go on to build the foundations of what we see today as Environmental, Social and Governance based investment.

It has forced issues such as climate change, human rights and telling the truth into the public consciousness. It’s difficult to argue with this wish-list. Why wouldn’t investors want better run companies who look after the environment, their staff, customers and are open and honest about how they do things?

We believe this issue is about more than ensuring future generations can breathe fresh air and have access to food and clean water, laudable as those aims are. It’s the opportunity for capitalism to shed its previous obsession with profit at any price and regain the public trust.

This momentum for change has come through the development of a series of Industry-based principles:

- Principles for Responsible Investment (PRI), established in 2006 by UNEP FI and the UN Global Compact, now applied by half the world’s institutional investors ($83 trillion).

- Principles for Sustainable Insurance (PSI), established in 2012 by UNEP FI and today applied by one-quarter of the world’s insurers (25% of world premium).

- Principles for Responsible Banking (PRB) launched on 22 September 2019, now with more than 130 banks collectively holding $47 trillion in assets, or one third of the global banking sector.

The goal of these principles was to harmonise previously discordant, competing groups and to create the most effective global knowledge sharing network amplifying the collective voice of the finance sector in policy debate. They engaged policymakers, regulators, and supervisors on the role of the financial sector in contributing to sustainable development supporting the UN’s efforts to build global consensus on “making the world a better place” for everyone.

Some of the UNEP FI strategies were highly effective in getting the attention of banks, whose purpose is to make money, and insurance companies, whose purpose is not to lose money. In 2011, the UNEP FI presented to large multi-national institutional investors highlighting their exposure to costs from environmental damages and initiated collective cooperation.

Later that year the subject of sovereign credit risk was under consideration with global institutions and governments exploring the link between ecological risk and country level risk. It demonstrated that there was a series of material and quantifiable risks that should be addressed.

So, we have proof that investment returns are damaged by poor environmental and social behaviour. In addition, we have measurable negative impacts on sovereign debt and global bond markets. Financial institutions recognised these risks could affect their ability to make money, and insurers identified risks that could cause them to lose significant amounts of money. This formed the basis for new thinking and risk management processes that went beyond simply poring over a company’s financial performance. It brought environmental, social, and operational governance practice to the table.

The concept of making the world a better, cleaner place has identifiable financial and social benefits it seems. Recent performance comparisons of “traditional” and high-scoring ESG shares suggest those high scoring shares produce better results, with lower risk. But what about the fixed income or bond market? It shows companies scoring well in ESG terms borrow money at lower rates, again giving them the advantage of lower funding costs. As always, there is much more to consider. Here’s a handy summary from Bank of America Securities research:

The surge in sustainable investing is global. The debate has moved from “will it underperform?” to “can investors afford not to take such issues into account?” Detailed analysis from Bank of America (ESG from A to Z: A Global Primer) found that companies with better ESG characteristics performed better financially within the time frames studied while those with poor records posed higher risks for themselves and for investors.

ESG has gone from niche to mainstream. Larry Fink, CEO of BlackRock, one of the world’s biggest financial managers with $7.4 trillion under management (2019 Annual Report), has put Corporate Sustainability at the top of his list. Here is BlackRock’s Mission Statement on Sustainability:

We are an asset manager whose objective is to create better financial futures for our clients and the people they serve. We aspire to be an industry leader in how we incorporate sustainability into:

- our investment processes and learning across the firm

- our stewardship of our clients’ assets

- our sustainable investment solutions offered to our clients; and

- the operations of our own business.

Since January 2020 investment inflows have beaten expectations. The question was asked at a recent webcast, “What’s causing the sustainability wave?”. Jean Boivin, Head of BlackRock Investment Institute responded:

“I think at the root of it, it’s the changing preference of society or a greater awareness of what the risk might entail going forward.” Further adding “The bottom line is this a long-term phenomenon that is going to play over years and decades. Demand and capital reallocation are only starting and will be moving slowly over time. It means that we have now a new source of return across all asset classes and that will determine or change the way we should be building portfolios going forward.”

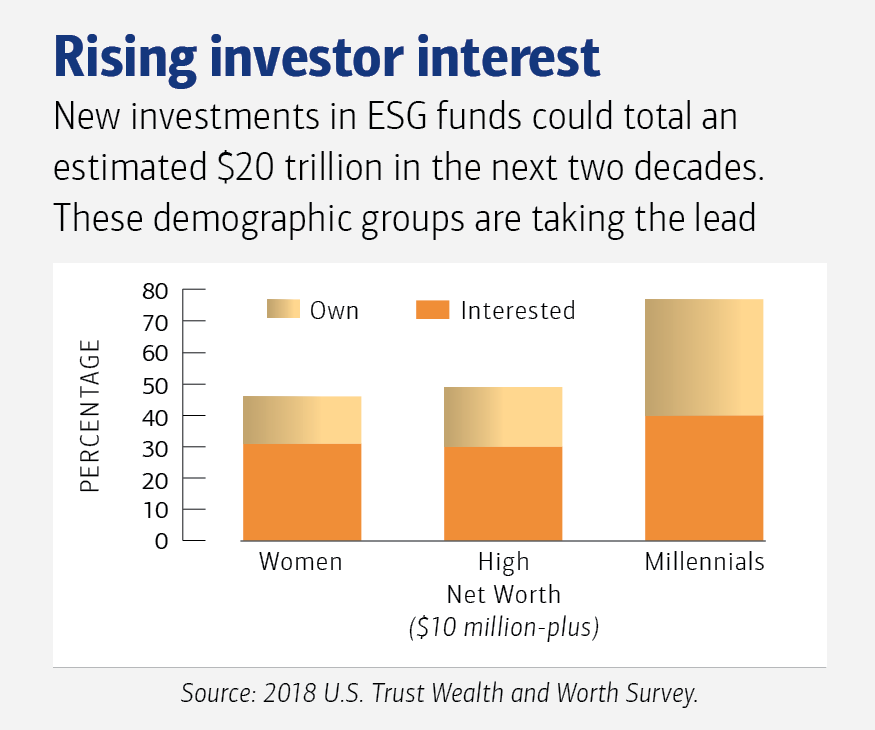

Savita Subramanian, Head of US Equity & Quant Strategy and Global ESG Research for BofA Global Research, estimates that the amount invested in ESG funds could rise by $15 – 20 trillion over the next two decades. “That’s equivalent to the size of the S&P 500 today,” she noted.

European investors represent almost half of the current $30.7 trillion of investable assets in sustainability funds, according to the Global Sustainable Investment Alliance. Awareness of ESG is on the rise among investors and companies in the United States. The Global Primer points to a “sea-change in U.S. corporate responsibility,” where companies are recognizing the importance of investing in employees, taking care of the environment, and other issues.

Further helpful comment comes from a paper from PIMCO, one of the largest credit and fixed interest managers which listed the following points in a “Why ESG” opinion piece.

- Good governance is systemically important. The financial crisis of 2008 was a wake-up call for public and private sectors, demonstrating how issues of culture and conduct could have systemic importance. Improving corporate governance is increasingly a goal for regulators and for fixed income and equity investors through active ownership.

- Public-private partnerships are expanding. Public-private collaboration has grown from addressing infrastructure and housing needs to tackling broader social and environmental issues. The U.S. municipal market and the European agency market are two examples of how government vision has enabled private capital to drive social investments.

- Climate change is a reality. Climate change is now universally understood and (almost) universally acknowledged. Mitigation techniques include international agreements such as the COP21 Paris agreement, which aims to keep the rise in world temperatures below two degrees, and private initiatives such as sustainable investment portfolios and more disclosure of climate-related financial risks.

- Energy sources are shifting. Climate change aside, there is a transformation occurring in energy markets. Well-telegraphed supply and demand drivers are shifting the dynamics of the oil market, natural gas is now cheaper than coal, and renewable energy sources are becoming cheaper and scalable.

- Technology is changing what we demand and how we consume. Whether it’s driverless cars in autos, smart metering in utilities, renewables in oil and gas, online sales in retail, or robo-advisers in asset management, most sectors of the economy are seeing paradigm shifts in the way business is conducted. Companies with ample resources and willingness to adapt will outperform, but others are likely to put investors at risk.

- Social media is driving convergence in social norms. Given its borderless nature, social media has the potential to alter the cultural blueprint of countries, and for investors, its effects vary from changes in individual consumer preferences and traditional election patterns to subsequent demands for new regulations.

- We are living longer. By 2050, there will be 2.3 billion people in the world over age 65, according to the United Nations. With average life expectancy rising in developed countries, sustainability issues will affect not only our children but also our older, less-capable selves. Climate change, income inequality, healthcare and poor governance are increasingly personal as they directly affect financial security in retirement.

- Demographics are changing. Millennials and Generation-X are increasingly taking over from Baby Boomers in positions of influence, changing business, financial and political landscapes. The newly formed French government is an example – half of its members are women. Younger generations are driving the fast growth of the “green bond” market and the field of sustainable finance in general.

- Regulation is providing tailwinds. ESG considerations have driven new regulations in a growing list of countries, which is tangibly affecting credit fundamentals. Examples include the shutdown of nuclear power in Germany, the Supervisory Review and Evaluation Process (SREP) in Europe, which governs subordinated financial debt, and France’s mandatory reporting of climate risk, which raises the bar for financial institutions.

- Value chains are global. Large corporations’ value chains are increasingly global. These value chains are complex and if poorly managed can prove costly. Investors can be quick to punish companies for child labour practices, human rights issues, environmental impact, and poor governance.

In summary, we continue to develop our investment philosophy and processes with ESG in mind. We are reviewing our True Wealth portfolios with a view to expanding ESG content.

Demand continues, especially among younger generations who are vocal in their demands for more control and purpose for their invested wealth:

The fears expressed initially have proved unfounded as ESG funds have been better supported by investment inflows, with a noticeable migration from more traditional funds. Performance, especially over the extremes experienced this year, has been better than expected.

While environmental social and governance considerations may have once been viewed as distracting sideshows compared to the main event of making money, they have now become the headline act. Investor audiences are voting with their feet and their wallets, preferring this more considered style and sensitive performance. This show may well run and run.

This document is intended to provide information for existing clients of Stewardship Wealth on the subject matter. Any reference made to specific funds should not be construed as financial advice or a recommendation to buy or sell any investments. You should never make an investment without receiving appropriate advice or undertaking your own research. Stewardship Wealth clients will receive a personal recommendation based on their personal financial circumstances. It goes without saying, but as we know ‘investments can fall as well as rise and you may get back less than you invested’ as well as ‘past performance is no guarantee of future performance/returns.’ If you are not a Stewardship Wealth client and would like to know more about how we advise our clients, please contact us at: Hello@stewardshipwealth.uk