“Reality is merely an illusion, albeit a very persistent one” – Albert Einstein .

I’m sure there are many of us that remember the following mind-bending quote.

“There are known knowns. These are things we know. There are known unknowns. That is to say, there are things we know we don’t know. But there are also unknown unknowns. These are things we don’t know we don’t know.” – Donald Rumsfeld, former US Secretary of Defence.

Thinking you know something without supporting evidence can really hurt a business.

Consider the friction created by thinking you know your clients, when in reality you don’t. You may even make a significant change to your business model. You may even believe it would be a great idea to buy or merge with another business. Even worse you could sell your business to a new owner all without knowing how your clients will react.

Change is virtually impossible to deliver unchallenged. Sydney J Harris, an American journalist and columnist, summed it up brilliantly when he wrote, ”Our dilemma is that we hate change and love it at the same time; what we really want is for things to remain the same but get better.”

Stewardship Wealth actively participates in client surveys to ensure we really know our clients. We want to be sure about their values, attitudes and expectations. We want to know what they value about the things we do. Our Concilium meetings, where we gather a group of clients together to discuss issues, gives us the added advantage of hearing first hand from clients their opinions when we share our plans. We also get to talk about ideas we believe will improve our service, and receive immediate feedback, both positive and negative.

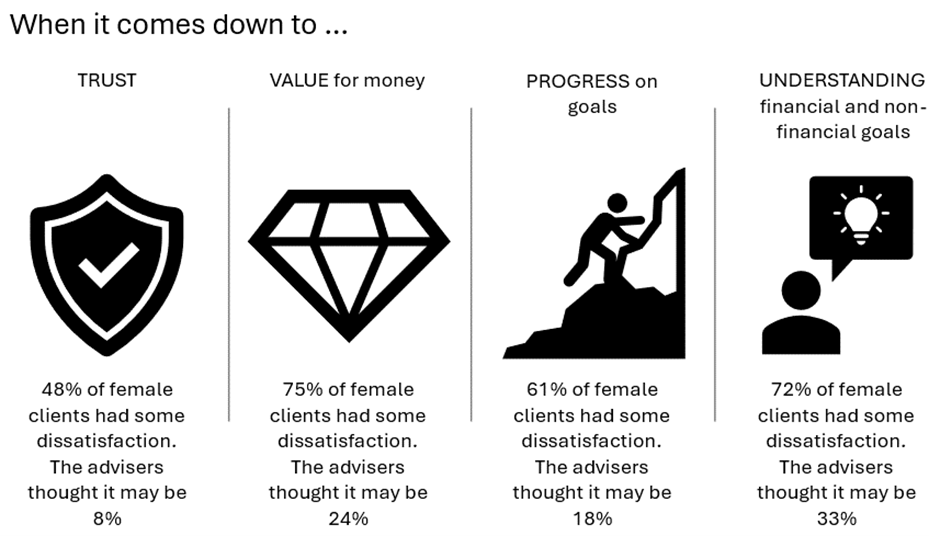

Recent research by Schroder and Ad Lucem, a financial services thought leadership collective, highlighted the dangers of advisers mistakenly believing they really knew their clients.

Here’s the background. Almost ten years ago the Centre for Economics and Business Research issued the results of a study suggesting that by 2025 over half of the wealth in the UK would be controlled by women. The transfer of wealth from ageing baby boomers was more likely to be from a deceased male to their female spouse or partner.

Truly understanding the health of your relationship with your clients, is vital. What Schroder and Ad Lucem’s research found was that there was a significant disconnect between what businesses believed about the strength of their client relationship, and their clients’ opinions. Here are some of the study’s findings.

The big question was, “If your partner were to die, would you stay with your existing financial adviser?” When asked, only 34% said they would, yet their advisers assumed 62% would retain their relationship with the business.

“The customer’s perception is your reality.”- Kate Zabriskie.

Such a gap between the adviser’s perception and the facts is alarming. Trust and understanding financial and non-financial goals form the foundation of any working relationship. It is inconceivable clients would stay with a financial planning business they didn’t trust.

Unsurprisingly women value things differently from men. Women want someone they can trust, delivers value for money, peace of mind, and progress towards their goals. They regard spending time discussing both financial and non-financial goals as important.

Men tend to lean towards investment performance and are less likely to seek advice as they often appear more confident in their own ability.

By comparison women prefer to take less risk and be more diversified, choosing not to make too many changes to their portfolios, but taking a longer view. They are also less likely to chase “hot stocks” which often results in highly concentrated, higher risk portfolios. Interestingly research also shows that women often enjoy better returns than men.

Here are some other findings:

- 29% of advisers thought that women would find managing their finances on their own difficult. In reality, only 9% of women felt it would be challenging.

- 45% of advisers said their main contact was with the male client, 22% always made sure both partners were present. And 66% of advisers said it was difficult to engage with both partners.

All of this is good news for financial planners who take time to meet with their clients regularly, who actively listen, understand and address their concerns as well as updating them on their progress. It makes sense for planners to encourage both partners to attend all meetings whenever possible, and communicate in a way that both clients can understand.

“The more you engage with customers, the clearer things become and the easier it is to determine what you should be doing.” John Russell.

We know this is only achieved through time, experience, patience and effort. Every time we meet with you, we aim to come away from the conversation better. Better informed, better equipped and more aware of your opinions, and expectations. We believe it’s good to talk, as the late Bob Hoskins used to say.