Suddenly my inbox is filled with financial predictions from the seers of the City. It takes me back to the years presenting our (Pru M&G’s) views for the year ahead. These are dangerous predictions to make, and seldom if ever correct. As Yogi Berra, the legendary baseball player and coach, famously said, “It’s tough to make predictions, especially about the future.”

As if proof were needed, at the end of 2023 a number of major US investment managers made the following predictions about the US S&P 500 index return for 2024. Here are the highlights:

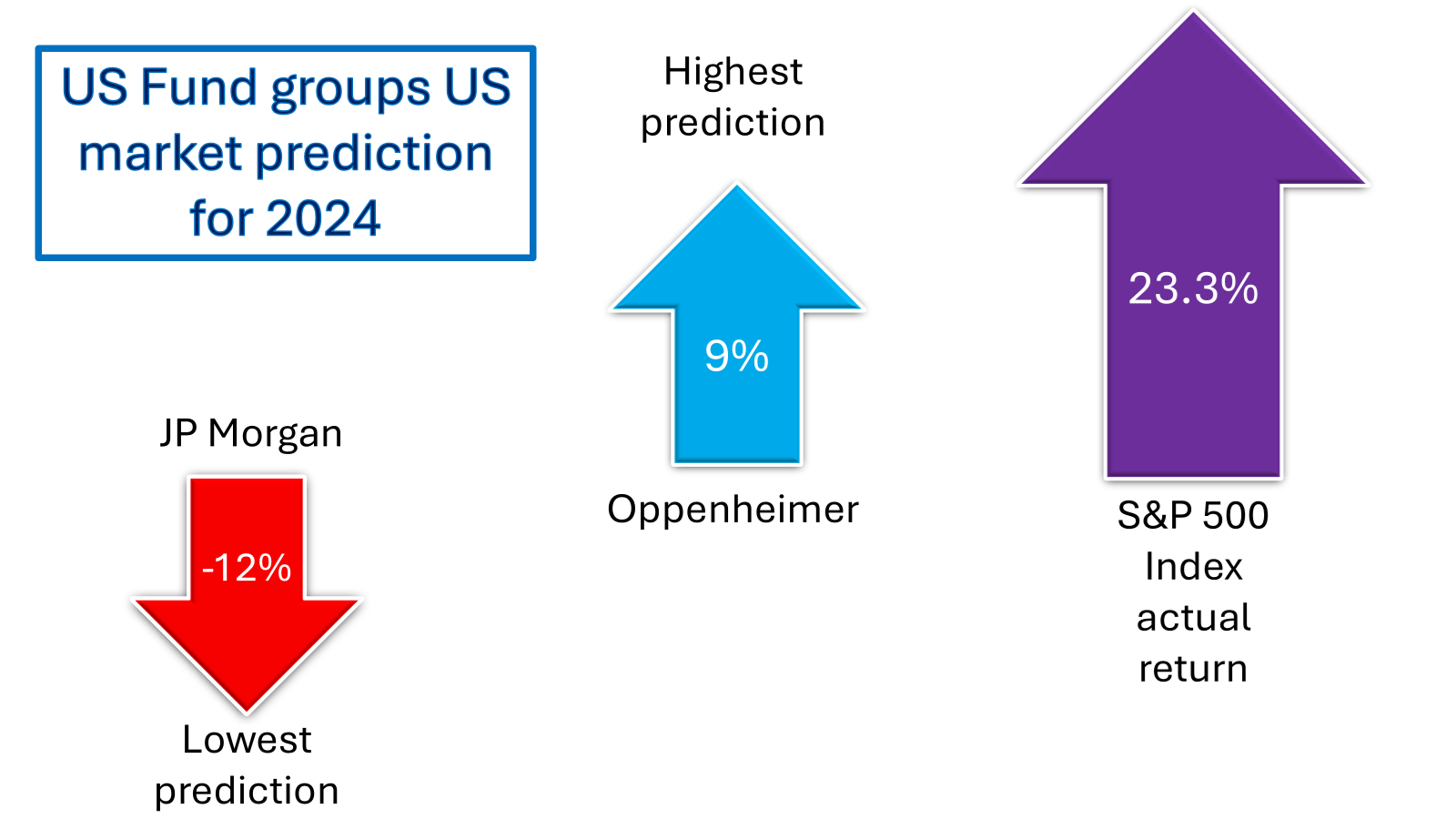

The most positive, or bullish* to use industry jargon, was Oppenheimer who predicted it would rise by around 9%. The most negative, or bearish*, which was JP Morgan, suggested it would be down -12%. It actually rose 23.3%. Oops.

- JP Morgan’s original prediction issued in October 2023 was, “We expect downside for equites from current levels”. Mid-year it had changed to, “The US economy should continue to provide a rising tide to support most investment boats for the rest of this year and into 2025”.

- Fidelity’s November 2023 message was, ”Barring something extraordinary, next year we expect to see the economy finally turn lower”. In June 2024 this had changed to, “What we are seeing in the US is a resilient expansion.”

It seems that sorry seems to be the hardest word when explaining to investors why experts backed up by teams of researchers and analysts got things so wrong.

AJ Bell, an investment manager and platform company, created its own Manager versus Machine report. It reviews the outcomes of a range of seven key global share markets. Unsurprisingly, it found that two-thirds of active funds, those that are based on market prediction and in-house research, didn’t beat a typical index fund. This suggests it would have been better to buy the index fund, save money, reduce risk, and enjoy a higher return.

However, not every active fund underperforms the index. Some do better, but not every year. This for me calls into question their continued belief in their research, investment process and decision making. There are some famous names in the industry with well-deserved reputations as top performing fund managers. Recently, Nick Train, a popular star fund manager, faced the public and… let’s just say it didn’t go well. He was very open and honest saying, ”I’m running out of ways to say sorry for poor performance.” To be fair, over the long-term, Nick Train has a strong performance record, but like every other active manager they go through tough times.

Consider this. It is impossible for all active managers to outperform the index. An index is simply a list of companies normally ranked . The market capitalisations are made up of the number of shares available to buy, multiplied by the share price. The market is simply an electronic trading floor. Share trades require buyers and sellers. You can only buy what someone else is prepared to sell. There must therefore be a in every trade.

An oversimplification I know, but at the end of every period there are those who bought the right shares, at the right time and saw values rise, and those who sold those shares at the wrong time and saw prices fall, losing out as a result. The aim of any active fund is to outperform the benchmark index. It also needs to outperform by enough to cover the extra costs over those of an index tracking fund. It makes beating the index harder work, not impossible, but means you have to be on the right side of most of your share purchases, and your sales, and your timing. A real challenge.

We remain confident that an evidence-based investment philosophy is the most appropriate solution for our clients. We’ll leave informed speculation to the alleged “experts”.

* A little aside…