Index tracker fund popularity continues to grow principally because they provide access to a diverse range of investments at low cost. But how do index trackers work?

First, what is an index? An index is a statistical measure that tracks the performance of a group of assets, such as stocks, bonds, or other financial instruments. It is used to represent the overall performance of a specific market or sector. Indices are designed to give investors a snapshot of how a market or segment of the market is performing, making them useful benchmarks for comparing individual investments. The UK’s FTSE 100 index is probably the best-known index for UK investors. It is a measure of the value of the 100 largest UK registered companies with ‘publicly available’ shares you can buy (this ‘publicly available’ label is important as we shall see later).

It is “rebalanced” each March, June, September and December. The largest companies stay put, and those whose values have been overtaken by others fall out. The process is rules driven, rigid and mechanical. Right now, some of those rules are causing some difficulties among US index trackers.

Here’s how Apple shook up the US indices rebalancing process. Warren Buffett is Chairman and CEO at Berkshire Hathaway one of the world’s most successful investment companies. Over the past 12 months he unexpectedly sold half his holding in Apple. A small matter of 390 million shares reportedly worth $75 billion.

In effect, Apple’s weighting in the range of index benchmarks has been understated. As these shares were held by Berkshire Hathaway, they were not ‘publicly available’ but classed as institutional investments. This means they do not count towards the weightings of shares in the index. This, in terms of the S&P 500 (the stock market index that tracks the performance of 500 of the largest publicly traded companies in the United States), meant only 96% was publicly available. Usually this would be a minor rounding issue, but replacing a small percentage of a $3.3 trillion company is a little more complicated. It also ushers in unintended consequences.

For example, US index tracking funds will be forced into making up the difference from 96% to 100%. This means index trackers buying an extra $40bn worth of Apple shares to replicate the new index weightings later this month. The 20th of September is the next date for the S&P 500, amongst other indices. But there is more. It affects other index constituents too. Index funds are compelled to sell down their share weightings to make room for more Apple stock. So, some companies will see significant share sales simply due to the mechanical application of index rules.

One key factor at play is that funds tracking those indices will all carry out their buying and selling trades at a specific time, on a specific day, in a specific volume. This has some predictable outcomes. It leads to one of the highest-volume trading days of the year, often precipitating sizeable price movements and volatility. Research shows that share prices of those companies due to enter the index, tend to rise ahead of their addition while the price of those due to leave falls. Soon after the rebalancing this often reverses with risers falling back and fallers recovering.

As Joel Schneider, Deputy Head of Portfolio Management at Dimensional Fund Advisers puts it, “Index funds are systematically buying at temporarily high prices when they’re adding and selling at temporarily low prices, which is the opposite of what you’re supposed to do as an investor, they’re doing the exact opposite because of their own mechanics.” Add in the implementation costs for good measure. If only they could spread the trading frenzy over a few days and avoid the immediacy premium demanded to fulfil their obligations.

However, there is much more to index funds than meets the eye. You would assume that index funds tracking the same market or sector would deliver the same returns. Afterall they are all doing the same thing…aren’t they?

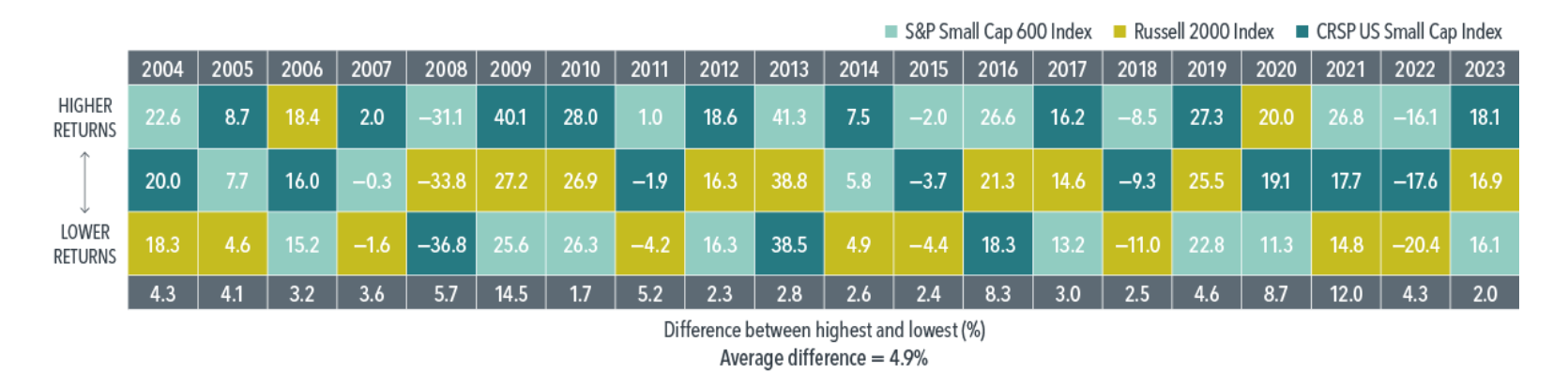

A recent Dimensional research paper compared the S&P Small Cap 600 index, Russell 2000 index, and CRSP US Small Cap Index returns over a 20-year period. The table below highlights the results. You could expect small differences due to different charge levels, but the figures are surprising. Standout years are 2009 where the gap between best and worst was 14.5%, and 2021 when the difference was 12.0%.

Which US Small Cap Index Is Passive?

Annual returns (%), 2004–2023

Source: Dimensional

How tracker funds are constructed and maintained differs across providers. This has important implications for the returns they produce. These return differentials also appear in funds tracking total US market benchmarks. Sample returns varied from 0.2% to 3.2% pa.

So, what conclusion can we draw from all of this? Firstly, Index trackers are not all the same. Their actions in replicating an index involve a range of different approaches. There are different levels of charges, different stock selection timing and trading practices that create hidden costs and are likely to impact on returns.

Tracker funds are not really passive in the purest sense. There is an element of active decision-making by necessity. Indices are not designed as investments. They are indicators that measure the performance of a market or sector of the market is performing. Trying to replicate it with precision is challenging, and as we have explored, the reconstitution and rebalancing mechanism is rules-based and mechanical. It creates a trading frenzy that has real cost implications for investors.

While trackers have their place in portfolios, our core belief is that an evidence based, scientific approach backed by decades of award-winning research is best placed to deliver the returns our clients expect.